When it comes to mobile payments, the U.S. is still well behind the curve, and this extends to all areas of mobile payments. But what is happening here, and now, are small merchants.

When it comes to mobile payments, the U.S. is still well behind the curve, and this extends to all areas of mobile payments. But what is happening here, and now, are small merchants.This week, Intuit unveiled GoPayment for Android 3.0 in NYC - more than a month after its preview in Barcelona last month at Mobile World Congress.

Intuit is venturing into the space for low cost, small merchant payments that Square has established on the iPhone and iPad platform and extended to Android. Square will send you the little square card reader for free, and swipes will cost you just 2.75%. Quite a bit less expensive and far more efficient than other methods of accepting cards, and far, far better than (shudder) PayPal.

Intuit is venturing into the space for low cost, small merchant payments that Square has established on the iPhone and iPad platform and extended to Android. Square will send you the little square card reader for free, and swipes will cost you just 2.75%. Quite a bit less expensive and far more efficient than other methods of accepting cards, and far, far better than (shudder) PayPal.

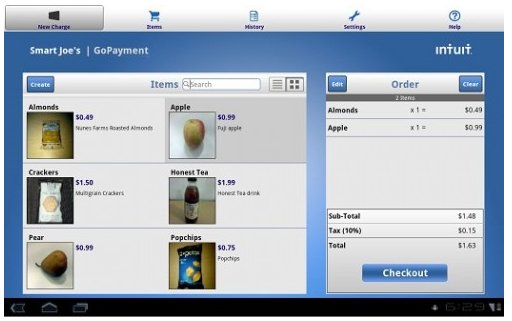

As we can and will reach the unbanked through mobile phones on the retail side, on the merchant side Intuit would like to compete for small businesses without merchant accounts, using banks that can't, or won't, help them. Intuit has targeted tablets, rather than phones, and loaded GoPayment for Honeycomb (Android 3.0) with features, so you can:

- Swipe cards within seconds – Save time and money by swiping a card instead of entering numbers manually. GoPayment features support for a variety of credit card readers. All compatible card readers also encrypt the credit card data for added protection.

- Authorize transactions with touch screen signature – For added security and professionalism, customers can quickly sign a tablet’s touch screen to authorize their transactions.

- Drag and drop frequently sold items from a product list – Quickly complete a sale by dragging and dropping items into the shopping cart and easily add or delete items as needed.

- Take photos of frequently sold items – Using a device’s camera, save time by photographing products and storing details to create a visual product list to quickly take customer orders.

- Find data quickly – Find items in a product list or locate past transactions using new search capabilities.

- Work within an easy-to-view, large-screen environment – Easily view transactions and work faster when processing payments on a tablet. GoPayment is optimized for tablet form factors building on Honeycomb’s “fragment” technology.